Regtech, fintech, insurtech, govtech… same, same but different? Over the years, we have seen the emergence of technology applied solutions, tailored for modern challenges. Financial Technology solutions (fintechs) is the precursor to a myriad of declinations.

Unsurprisingly, with the resurgence of regulatory pressures, the management of regulatory processes within the financial industry through technology (regtech) has been booming.

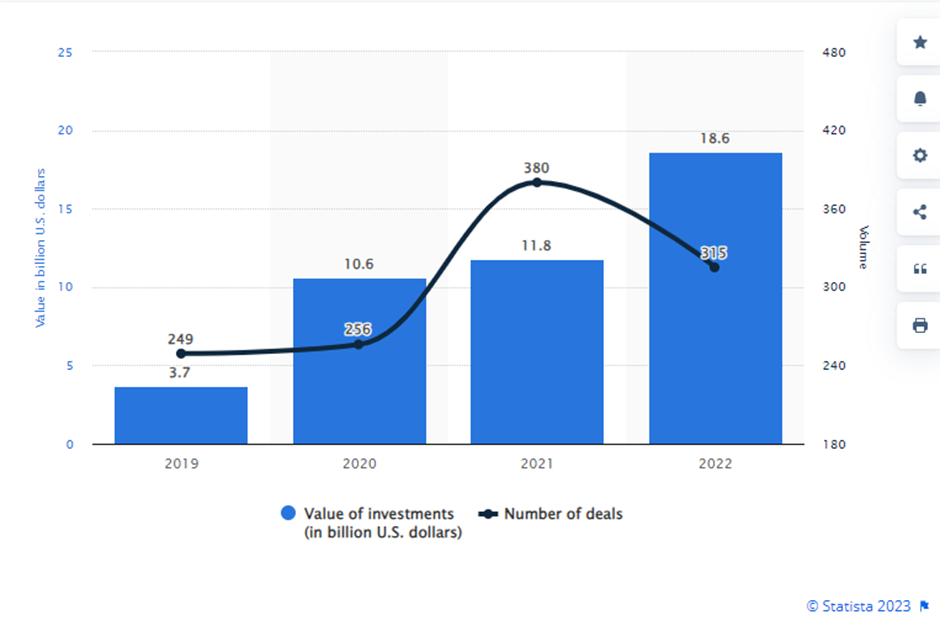

Interestingly, a 2023 study (Statista) revealed “in 2022, the total value of venture capital, private equity, and M&A investments in the Regtech sector worldwide was 18.6 billion U.S. dollars, which was a notable increase compared to the 11.8 billion U.S. dollars in 2021.

The number of deals, on the other hand, decreased slightly, from 380 deals in 2021 to 315 deals in 2022. The increasing value of investments is particularly surprising, considering that the value of investments into the fintech sector in general decreased significantly in 2022.”

Total value and number of venture capital, private equity, and merger and acquisition (M&A) investment deals in regtech worldwide 2019 to 2022

It is estimated regtech investments will reach US$22.3 billion by 2027. Examples of regtech investments worldwide are staggering. In the last six months alone:

- United Kingdom based eflow Global has raised £7 million in a Series A funding round.

- Corlytics has made its second acquisition of the year with the takeover of compliance policy mapping provider Clausematch. It follows the buyout of SparQ, a regulatory monitoring platform spun out of ING, in a €5 million aggregate deal sealed in January.

- Vilnius-based startup Amlyze, has concluded a $1 million pre-seed investment round.

There is a real market for regtech solutions, so why are we not seeing growth here in New Zealand? From a New Zealand perspective, the number of regulations we are subject to is not necessarily proportional to our size. On the contrary, our banking industry, for example, has to comply with New Zealand Regulatory obligations, and often Australian Prudential Regulation Authority’s (APRA) mainly due to parental ownership, as well as some European and American legislations. This includes the General Data Protection Regulation (GDPR), Foreign Account Tax Compliance Act (FATCA) and the Dodd Frank Wall Street Reform and Consumer Protection Act. So, if we are subject to local and international legislation, it seems logical to also have a need to be as automated as our global peers.

To illustrate the dichotomy found in the New Zealand regtech environment:

- Main sub-sectors of focus for New Zealand Trade and Enterprise (NZTE):

- Agritech

- Cleantech

- Healthtech

- Fintech

- RegTechNZ is represented as a working group of FinTechNZ, but regtech also applies to all other sectors as regulated entities

- In the New Zealand FinTech Ecosystem 2022: only six companies are categorised as regtech.

Legitimate questions worth considering include:

- Is there a confusion between fintech and regtech as categories?

- Fintech is intended to provide technical solutions for finance companies,

- Regtech is more specific in the use of technology to effectively and efficiently solve regulatory and compliance requirements.

- Why is there so little appetite for regtech growth in New Zealand despite a very active legislative and regulatory environment?

- What is needed to develop more technology tools purposely created to relieve local regulatory pressures?

By Emilie McCallum, Partner, Mosaic FSI, RegTechNZ working group partner

If you would like to know more about RegTechNZ, please connect with us online or follow RegTechNZ on LinkedIn.